5. Tata Steel

Tata Steel is the world’s eleventh-largest steel company, with an annual steel manufacturing capacity of 31 million tonne (MT). It is also the largest private-sector steel company in India measured by domestic production. The company has been an important player in the economic and industrial development of India and is also spreading its wings fast on the global stage, especially after the acquisition of European steel major Corus in 2007.

Over the past 10 years, Tata Steel has grown its net sales and profits at an average annual rate of 16% and 29% respectively. In other words, its sales and profits have multiplied by over 4 times and 12 times respectively during the past 10 years. The company has also maintained a relatively safe balance sheet over these years, except some concerns that crept in post the massive price it paid to acquire Corus. Tata Steel has also generated high return for shareholders, with its return on equity averaging over 30% during the past 10 years. Tata Steel has set an ambitious target to achieve a capacity of 100 MT of annual steel production by 2015. As per the company, this would be taken care by expansion of existing facilities in India plus global acquisitions.

Here is a simple model I’ve created to showcase what all goes into the creation of free cash flow for a typical steel company. Free cash flow, as you know from our past discussions, is what ultimately creates shareholder value. This chart will help you understand the working of Tata Steel and also serve as a helpful tool in analyzing other steel companies.

Keeping in mind the simplicity aspect that is otherwise missing in other company analysis reports you would come across, I’ve analyzed Tata Steel by answering 25 important questions that span its:

- Business performance,

- Financial performance,

- Management quality, and

- Competition.

Before we move ahead, here are the symbols that I’ve placed against each checklist point and that will tell you at a glance whether I have a positive or negative view on that particular point.

Indicates my positive view

Indicates my positive view Indicates my negative view

Indicates my negative view Let’s get started.

A. Business

1. Can I, in one sentence, say exactly what the company does?

Yes. Tata Steel manufactures steel, which is a key raw material used in the infrastructure, construction, automobiles, and consumer durables sectors.

2. Is it in my circle of competence?

Yes. Based on the shareholder value creation model I’ve shown above, it is easy to understand the business of Tata Steel. It is thus in my circle of competence.

3. Is it a low risk business?

No. Steel is a commodity business, and is highly cyclical in nature. The growth and profitability of a steel manufacturer like Tata Steel is highly dependent on the growth of Indian and global economy and capital expenditure by companies from other sectors like automobiles, consumer durables, and construction. And as you have seen over the past few years, things have been topsy-turvy for all these industries.

The profits of a cyclical business (like Tata Steel) are normally much higher during economic booms than during recessions. So it’s nearly impossible to take a call on the short to medium term future of such a business.

As far as Tata Steel is concerned, while the company has also faced the brunt of cyclicality in the past, it has still benefited on account of its large scale of operations and raw material linkages (as we will study below) that have helped it manage is operating margins in a much better way than its competitors.

4. Does the business have high uncertainty?

Yes. The business cycle in which Tata Steel operates is highly cyclical, as we have discussed above. And high cyclicality brings with itself high uncertainty. Cyclical companies are at the mercy of the economic cycle. While it is true that good management and the right strategic and business choices can make some cyclical firms less exposed to movements in the economy (like has been the case with Tata Steel), the odds are high that all cyclical companies will see revenues decrease in the face of a significant economic downturn.

5. Is it a good business?

Yes, but only if you a big enough player to benefit from economies of scale plus if you have a tight grip over your raw material costs. Tata Steel stands tall on both these accounts, although its raw material advantage has somewhat diminished after the acquisition of Corus.

6. Has the business got an enormous moat?

Not enormous, but as I mentioned above, if you are a large player and have a good integration on the raw material front, you have a competitive advantage against other smaller steel companies. By raw material integration, I mean the raw materials that a steel manufacturer can source from its own resources (from its own iron ore and coal mines) instead of depending on external sources. A highly integrated steel company not only benefits from a constant supply of raw materials, but also insures itself against the volatile price fluctuations that are so usual in the iron ore and coal market. Thus, Tata Steel’s business has a good moat because not only is it one of the largest players in the steel manufacturing industry, it also sources a large part of its raw materials from its own mines.

See the following chart that shows the comparison of raw material costs for Tata Steel and India’s largest public sector steel company SAIL. As you can see, Tata Steel’s material costs are much lower than what SAIL pays…

Data Source: Ace Equity, Safal Niveshak Research

…and this is what has helped Tata Steel to earn far superior operating margins (on a standalone basis) than what SAIL has earned over the past 10 years.

Data Source: Ace Equity, Safal Niveshak Research

7. Is there room for future growth?

Yes. While steel manufacturing will remain a cyclical business, it will also continue to be an essential building block of infrastructure development around the world, and especially in the emerging markets like India that are looking to spend trillions of dollars on infrastructure over the next many years. Tata Steel, with its huge capacities and long history of execution will be a key beneficiary of this spending. But remember one very important thing – With commodity companies, there is one shared characteristic. There is a finite quantity of natural resources on the planet; if oil prices increase, we can explore for more oil but we cannot create oil. Similarly, there is a limit to which iron ore and coking coal – key raw materials for steel manufacturing – can be mined. This also limits the manufacturing of steel, and thus sales and profit growth for steel manufacturers like Tata Steel.

8. Does the business generate strong free cash flow?

The volatility in revenues for steel (and other cyclical) companies is generally magnified at the operating income level because these companies tend to have high fixed costs. Thus, such companies may have to keep mines and production capacities operating even during low points in price cycles, because the costs of shutting down and reopening operations can be prohibitive. This impacts profits and thus cash flows.

However, as far as Tata Steel is concerned, despite being a commodity business and thus highly cyclical in nature, it has managed its cash flows very well. For its standalone (India) business, the company has generated positive free cash flows for the past 10 years. Even if you consider its consolidated (India + global) business, free cash flows have been positive throughout, expect during FY09 and FY10 when the entire steel industry was in doldrums and Tata Steel was facing added pressure from its acquisition of Corus. The overall free cash position for Tata Steel looks comfortable.

Data Source: Ace Equity, Safal Niveshak Research

9. What is the bargaining power of suppliers and buyers?

High. Given the rising competition in the industry, both the suppliers (of raw materials) and buyers (of Tata Steel’s products and services) have seen their bargaining power rise over the years. Of course Tata Steel is insulated to some extent on the raw material front for its Indian manufacturing operations, its international businesses still depend on a large scale on external raw material sources. This leads to pressure on operating margins in case of a rise in material prices. B. Financial Performance

10. Does the business have a consistent sales and profit growth history?

Yes. Tata Steel has grown its standalone sales and net profits at an average annual rate of 18% and 48% per annum over the past 10 years, which is a decent pace of growth, especially given the cyclicality of the steel business. Also, during these 10 years, the company has not seen a single year of decline in sales, while its profit has declined just once on a year-on-year basis (in FY10). So it’s been a good performance from Tata Steel on the sales and profit growth front. As for its consolidated business (including Corus’s numbers), the company’s sales and profits have declined at a rate of 3% and 10% per annum over the past three years. But we must look at this in the backdrop of an extremely poor economic condition in the European markets. Overall, I’m comfortable with Tata Steel’s past track record on the sales and profits front, and see no reason why the company won’t be able to maintain this over the next 10-15 years as well.

Data Source: Ace Equity, Safal Niveshak Research

On a long-term average – yes. For recent years – no. As I mentioned above, Tata Steel has had a better control on its raw material sources in the past. This, combined with the economies of scale, has helped the company keep a tight leash on its operating costs. This has subsequently helped the company earn average operating margins of above 25% till about FY08, when it acquired Corus and the global crisis hit its business. During the current crisis period (FY08 till FY11), Tata Steel has averaged operating margins of around 12%, which are reasonable considering the gravity of the crisis. Overall, I am comfortable with Tata Steel’s ability to earn high and industry-beating operating margins.

Data Source: Ace Equity, Safal Niveshak Research

12. Is its operating cash flow higher than net profits?

Yes. Tata Steel’s consolidated OCF has been higher than net profits for 7 of the past 9 years thereby indicating a good management of its working capital.

Data Source: Ace Equity, Safal Niveshak Research

No. Tata Steel’s average debt to equity has been around 1.4 times over the past 10 years, thanks in part to the high debt it assumed to fund the Corus expansion, In the pre-Corus era, the debt to equity was more comfortable at around 1 time. Despite its debt equity ratio being higher than my general comfort limit of 0.5 times, considering that commodity companies generally have high debt to equity ratios, and that Tata Steel has one of the strongest balance sheets in the steel industry, I am reasonably comfortable on this account. However the company could make me even happier by reducing its debt in the future.

Data Source: Ace Equity, Safal Niveshak Research

14. Is the current ratio greater than 1.5?

Yes. Tata Steel’s average current ratio over the past 10 years has been 1.7 times, which is above the comfort zone. As a general rule, a current ratio of 1.5 or greater suggests that a company can meet its short-term operating needs sufficiently. However, a higher current ratio can suggest that a company is hoarding assets instead of using them to grow the business. While this is not the worst thing in the world to do, it is something that could affect long-term returns.

Data Source: Ace Equity, Safal Niveshak Research

15. Does the company have a good dividend history?

Yes. In terms of dividend payout (amount of dividend paid as percentage of net profit), Tata Steel has averaged around 25% over the past 10 years. This is a comfortable level from a shareholder’s point of view. 16. Is the Altman Z score > 3?

No. But it’s just there at 2.4, so the business looks reasonably protected against bankruptcy. Plus, this number does not capture the financial backing that the company has of its parent Tata Sons. Read more on the Altman Z-Score.

17. How capital intensive is the business?

High. Commodity companies like Tata Steel need a continuous flow of fresh capital to provide for the expansion of their manufacturing capacities.

The legendary investor, Warren Buffett wrote in his 1992 letter to shareholders – “The best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return. The worst business to own is one that must, or will, do the opposite – that is, consistently employ ever-greater amounts of capital at very low rates of return. Unfortunately, the first type of business is very hard to find.”

As such, even when Tata Steel has incrementally employed large amounts of capital in the past, it has been able to earn a reasonable rate of return on this capital (of above 25%), which, despite falling in recent years, has a good probability to rise to higher levels given the company’s strong capital allocation history.

18. Has it got a high and consistent return on capital and return on equity?

These ratios were more consistent in the pre-Corus and pre-2008 days. However, since the trouble started in 2008, Tata Steel has seen a decline in its return on equity (RoE) and return on capital employed (RoCE). Over the past 3 years, while the average RoE has been 13%, the average RoCE has stood at 11%. As compared to this, the 10 year averages have been 32% and 26% respectively.

Data Source: Ace Equity, Safal Niveshak Research

C. Management Quality 19. Is the management known for its capital allocation skill and integrity?

Yes to both integrity and capital allocation skill. As far as its operating business is concerned, Tata Steel has a history of earning high return on capital. However, in recent years, the company has become overly aggressive in pursuing its global ambitions. This saw it buying the European steel major Corus in an expensive deal in 2007. This acquisition, combined with the global slowdown that has followed ever since, has led to Tata Steel losing its way on the return on capital front. However, if any Indian steel company were to get the top ranking for capital allocation in the long term, without doubt it will be Tata Steel.

As far as the integrity part is concerned, there’s no doubt that the company (along with most of its other group companies) are among the best in India when it comes to business integrity.

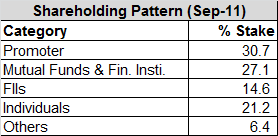

20. Is management shareholding > 10%?

Yes. Tata Steel’s chief promoter Tata Sons owns around 29% stake in the company. The total promoter group shareholding in the company stands at around 31%.

21. Has there been any substantial equity dilution in the past?

No. Tata Steel has had just two major equity dilutions over the past 10 years – first in 2004 when it issued bonus shares in a ratio of 1:2, and then in 2007 when it made a rights issue.

22. Are management’s salaries too high?

No. The combined salary of Tata Steel’s top three management personnel was Rs 8 million in the latest completed year (FY11). This is low by any standards of measurement of management compensation in India.

23. What has management done with the free cash in the past?

Tata Steel has employed part of its free cash flow towards dividend to equity shareholders. Its average dividend payout (dividend paid out as percentage of net profits) has been over 20% over the past 10 years, which is a good enough number for a company that has been on an expansion spree.

D. Competition

24. Does the business face high competition?

Yes. Competition for Tata Steel is global in nature.

25. Has the management focused on market share or profitability in the past?

Unlike firms in many other businesses, commodity companies like Tata Steel are, for the most part, price takers. In other words, even the largest commodity companies have to sell their output at the prevailing market price. Not surprisingly, the revenues of such companies will be heavily impacted by the commodity price. In fact, as commodity companies mature and output levels off, almost all of the changes in revenues can be traced to where we are in the commodity price cycle. When commodity prices are on the upswing, all companies that produce that commodity benefit, whereas during a downturn, even the best companies in the business will see the effects on operations.

Before I move into calculating the intrinsic or fair value range for Tata Steel, let me make one thing very clear. Intrinsic value isn’t a definite figure but just a ‘calculated’ value. In fact, the calculation of intrinsic value of a business mostly throws up a highly subjective figure. And this figure changes as estimates of variable like future cash flows are revised (given that the future is unknown).

Anyways, what I have done here is rather than arrive at a single intrinsic value figure for Tata Steel, I have calculated the value using 5 different methods and then arrived at a ‘fair value range’ for the stock.

1. Net present value based on a 2-stage 10-year DCF

The discussion about the calculation of net present value using a discounted cash flow model (DCF) can be found in the 7th lesson of my free course on investing – Value Investing for Smart People.

I have done a 2-stage DCF analysis for arriving at the intrinsic value for Tata Steel.

But as a reference, here is the formula for calculating the NPV:

Where:

PV = present value

CFi = cash flow in year i

k = discount rate

g = growth rate assumption in perpetuity beyond terminal year

TCF = the terminal year cash flow

n = the number of periods in the valuation model including the terminal year I have calculated Tata Steel’s future cash flow for the next 10 years, assuming 2 different rates of growth in cash flows of 8% (years 1-5), and 5% (years 6-10).

As for the discount rate, I’ve assumed it at 15% assuming the average cost of capital for the company.

As for the discount rate, I’ve assumed it at 15% assuming the average cost of capital for the company.My expected terminal growth rate for the company’s cash flows – expected growth in cash flow after 10 years and till eternity – is 1%. It’s important to remember one key factor here. There is a finite quantity of natural resources on the planet. There is a limit to which iron ore and coking coal – key raw materials for steel manufacturing – can be mined. This also limits the manufacturing of steel.

Thus, when valuing steel or other commodity companies, this factor (finite resources) will not only play a role in what our forecasts of future commodity prices will be but may also operate as a constraint on our normal practice of assuming perpetual growth (in our terminal value computations). So it’s important to assume a very low terminal growth rate for such companies. Taking this into account, I’ve assumed a terminal growth rate of just 1% for Tata Steel in my DCF calculation.

Based on these numbers and after reducing the net debt (debt minus cash), the present or discounted value of future cash flows for Tata Steel is coming at Rs 560 per share, which is also the stock’s intrinsic value using this method.

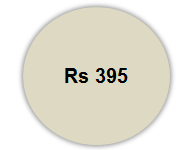

2. Earnings Power Value (EPV)

After DCF, the second most reliable measure of a firm’s intrinsic value is the value of its current earnings. This method is known as ‘Earning Power Value’ or EPV. This value can be estimated with more certainty than future earnings or cash flows, and it is more relevant to today’s values than are earnings in the past.

After DCF, the second most reliable measure of a firm’s intrinsic value is the value of its current earnings. This method is known as ‘Earning Power Value’ or EPV. This value can be estimated with more certainty than future earnings or cash flows, and it is more relevant to today’s values than are earnings in the past.The formula for EPV of a company is:

Here, ‘R’ is the cost of capital. Tata Steel posted an average adjusted EPS (earnings per share) of Rs 59 over the past five years (note here that I haven’t taken the latest year’s EPS as I did with L&T, but the average EPS of last 5 years given that this is a cyclical business).

Now, if Tata Steel’s profits were to stagnate and remain at Rs 59 per share going forward, and applying the EPV formula here, I multiply Rs 59 with 1/15% (15% is the approx. cost of capital for the company).

This gives me a value of Rs 395 per share, which is Tata Steel’s intrinsic value as per the EPV calculation.

3. Pricing relative to 10 year average P/E ratio

True value investors, as Graham has prescribed, won’t pay a price based on the stock’s latest P/E or the company’s latest earnings. They will take a much longer term view…as long as 10 years.

True value investors, as Graham has prescribed, won’t pay a price based on the stock’s latest P/E or the company’s latest earnings. They will take a much longer term view…as long as 10 years.Here, I have attempted to estimate the intrinsic value of Tata Steel using the company’s last 3 years average earnings, and last 10 years average P/E ratio. So the formula is:

Tata Steel’s average P/E ratio for the past 10 years has been around 8 times, while its last 3 years’ average EPS has been Rs 41 per share. Based on the formula, Tata Steel’s intrinsic value is coming to Rs 331 per share. 4. Graham number

Graham number is the formula Ben Graham used to calculate the maximum price one should pay for a stock. As per this rule, the product of a stock’s price to earnings (P/E) and price to book value (P/BV) should not be more than 22.5 i.e., P/E of 15 multiplied by P/BV of 1.5.

Graham number is the formula Ben Graham used to calculate the maximum price one should pay for a stock. As per this rule, the product of a stock’s price to earnings (P/E) and price to book value (P/BV) should not be more than 22.5 i.e., P/E of 15 multiplied by P/BV of 1.5.But why did Graham specifically used a P/E of 15 and P/BV of 1.5? Why didn’t he use some other numbers?

Well, he thought that nobody should be willing to pay more than the AAA bond yield at that time. AAA bond yield at that time was 7.5%. Therefore, AAA P/E was arrived at 1/7.5 or 13.3, which was rounded up to 15. Similarly he thought that nobody should pay more than 1.5 P/BV for a stock.

Graham insisted that the product of the two shouldn’t be more than 22.5. In other words,

(P/E of 15) x (P/BV of 1.5) = 22.5

Put another way:

(P/E) x (P/BV) = 22.5

Price(sqr)/(EPS x BVPS) = 22.5

Price(sqr) = 22.5 x EPS x BVPS

Take the square root of both sides, and you get the equation for the Graham Number.

As such, for Tata Steel, the Graham formula will stand as such:

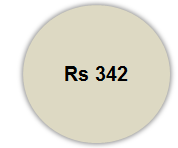

5. Pricing relative to 10 year average P/BV ratio

Price to book value or P/BV is a better valuation tool than P/E for valuing commodity companies like Tata Steel. This is for a simple reason that unlike earnings that are highly volatile for these companies, the asset base (represented by book value) is much more stable.

Price to book value or P/BV is a better valuation tool than P/E for valuing commodity companies like Tata Steel. This is for a simple reason that unlike earnings that are highly volatile for these companies, the asset base (represented by book value) is much more stable.I have attempted to estimate the intrinsic value of Tata Steel using the company’s last 10 years average book value per share, and last 10 years average P/BV ratio. So the formula is:

Tata Steel’s average P/BV ratio for the past 10 years has been around 2 times, while its last 10 years’ average book value has been Rs 171 per share. Based on the formula, Tata Steel’s intrinsic value is coming to around Rs 342 per share. 6. Dividend discount model

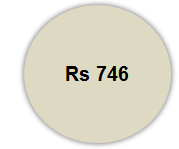

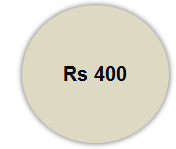

As we have discussed in the DCF method above, the value of a stock is worth all of the future cash flows expected to be generated by the firm, discounted by an appropriate risk-adjusted rate or discount rate. Now, as per the Dividend Discount Model or DDM, dividends are the cash flows that are returned to the shareholders.

As we have discussed in the DCF method above, the value of a stock is worth all of the future cash flows expected to be generated by the firm, discounted by an appropriate risk-adjusted rate or discount rate. Now, as per the Dividend Discount Model or DDM, dividends are the cash flows that are returned to the shareholders.Hence, to value a company using the DDM, you calculate the value of dividend payments that you think a stock will throw-off in the years ahead. Here is what the formula is:

The modified formula for valuing a company with a constantly growing dividend is…

Given that Tata Steel has paid higher dividends over the years, we use this ‘dividend growth’ formula for calculating the stock’s intrinsic value. Assuming a discount rate of 15%, dividend growth rate of 12%, and the latest dividend of Rs 12 per share, and inputting these numbers in the above DDM formula, I get to an intrinsic value of Rs 400.

Fair Value Range

We have calculated 6 different intrinsic values for Tata Steel using 6 different methods. So much for the ‘target prices’ you hear on business channels every day as if these were the holiest numbers!

We have calculated 6 different intrinsic values for Tata Steel using 6 different methods. So much for the ‘target prices’ you hear on business channels every day as if these were the holiest numbers! As you can see from the above calculations, the ‘target price’ isn’t such a holy number and can differ based on the method used to calculate it.

Anyways, based on the above calculated intrinsic values for Tata Steel, we can arrive at a ‘fair value range’ for the stock. Here is how I calculate it:

High End of the Fair Value Range = [Average of above four intrinsic values]

Low End = [(Average of above four intrinsic values) – (0.5) x (Std Dev)]

Based on this, the fair value range for Tata Steel’s stock is Rs 380 to Rs 460.

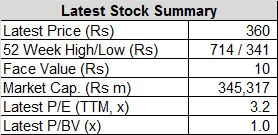

Assuming a margin of safety of around 25%, I would be comfortable buying Tata Steel’s stock at any price less than Rs 350. Given that the stock’s current price is just around this level, if I have surplus cash to invest, I will be happy to buy it at the current levels.

Given the overall weak scenario in the stock markets, the stock might fall further down from the current levels. But that is not what value investors are worried about when they’ve already taken into account an appropriate margin of safety.

Data Source: Ace Equity, Safal Niveshak Research

Data Source: Ace Equity, Safal Niveshak Research

Data Source: Ace Equity, Safal Niveshak Research

Labels: Safal Niveshak

posted by Arthur Lobo (Keyboardist/Vocalist/Composer) @ 2:49 AM

6 Comments

![]()

6 Comments:

Awesome blog. And very informative also. MS chequered plate

Tata Steel's achievements are commendable. I invite you to visit our site at UNS C71500 Fasteners explore our diverse steel solutions.

Tata Steel's impact is undeniable. If you're passionate about steel, check out our website for the best Stainless Steel 304 Fasteners.

"I found your article about Tata Steel quite informative. If you're interested in S355G10+M Sheets products, take a look at our selection on our website. You won't be disappointed!"

"Your article about Tata Steel is quite comprehensive. If you're in need of ASTM A790 Duplex 2205 Pipe products, feel free to explore our offerings on our website. We have Pipe products for every industry !"

"Your article on Tata Steel is informative. If you're in search of Stainless Steel 304 Flange products, don't forget to explore our range on our website. We have a variety of options available."

Post a Comment

Subscribe to Post Comments [Atom]

<< Home